Table of Content

Your debt-to-income ratio will go down and you may even get a nice bump in your credit score. ” That’s because even with all the angst involved in applying for and being approved for a home loan, lenders are often inclined to loan you more money than you expect. While it might be harder to get a mortgage with a low income, itâs definitely possible. There are several types of loans specifically geared toward low-income borrowers, such as FHA, USDA and VA loans as well as Fannie Mae HomeReady loans and Freddie Mac Home Possible loans.

The calculator will then reply with an income value with which you compare your current income. Mortgageloan.com is a product of ICB Solutions, a division of Neighbors Bank. ICB Solutions partners with a private company, Mortgage Research Center, LLC, (nmls # 1907), that provides mortgage information and connects homebuyers with lenders. Neither Mortgageloan.com, Mortgage Research Center nor ICB Solutions are endorsed by, sponsored by or affiliated with any government agency. ICB Solutions and Mortgage Research Center receive compensation for providing marketing services to a select group of companies involved in helping consumers find, buy or refinance homes.

How much mortgage payment can I afford?

Lenders will thoroughly evaluate your income and assets, credit score, and debt-to-income ratio. Note that you can adjust the loan amount and interest rate by using the sliding indicators; left-click and hold on the green triangles to adjust the figures. As you do, the required income level and monthly mortgage payment will immediately change as well. With home prices hitting record highs, you might wonder whether now is even a good time to buy a house. It’s important to focus on your personal situation instead of thinking about the overall real estate market. Is your credit score in great shape, and is your overall debt load manageable?

For example, let’s say that you could technically afford to spend $4,000 each month on a mortgage payment. If you only have $500 remaining after covering your other expenses, you’re likely stretching yourself too thin. Remember that there are other major financial goals to consider, too, and you want to live within your means. Just because a lender offers you a preapproval for a large amount of money, that doesn’t mean you should spend that much for your home.. A house is one of the biggest purchases you can make, so figuring out how much you can afford is a key step in the home-buying process.

Where to get a personal loan?

It’s important to consider all the factors needed to apply and where you stand. Focus on meeting all the necessary expectations of the lender and being sure that you can meet all payments on-time before submitting the application. A history of no late payments will make you look good in the eyes of any lender.

Others allow prospective borrowers to apply over the phone or in person at a physical location. However, lots of debt, a history of previous foreclosures, and a low credit score can slow down the process. If any of these apply to you, the pre-approval process can be much longeranywhere from a few days to several monthsdepending on the complexity of your finances.

What To Do If You Cant Get Preapproved

They do not perform hard inquiries on your credit report, which means it does not affect your credit score. Mortgage insurance typically costs 0.5 – 1.85 percent of your loan amount per year, billed monthly, though it can go higher or lower depending on your credit score, down payment and length of your loan. Lenders examine your debt-to-income ratio, credit score, and ability to repay the mortgage to see if you qualify for a home loan. The best way to determine if you qualify is to connect with a mortgage lender and get pre-approved.

These loans have competitive mortgage rates, and they don't require PMI, even if you put less than 20 percent down. Plus, there is no limit on the amount you can borrow if you’re a first-time homebuyer with full entitlement. You’ll need to also consider how the VA funding fee will add to the cost of your loan. Your credit score is the foundation of your finances, and it plays a critical role in determining your mortgage rate. For example, let’s say you have a credit score of 740, putting you in the running for a rate of 4.375 percent on a loan for a $400,000 property with a 20 percent down payment. If your credit score is lower — 640, for example — your rate could be higher than 6 percent.

Mortgage pricing explained

A specialist underwriter combs through the paperwork, checking for red flags and hidden risks. And you may need to renew yours several times during the house-hunting process. The last thing you want to do is find your perfect home, make an offer, and then discover your letter’s expired. Mortgage preapproval is the very first stage of the home buying process. It’s basically a trial run that will tell you how likely you are to get approved for a mortgage and how much you’re qualified to borrow.

Thirty-year fixed-rate loans are the most widely used home financing tool in the country. In August 2020, 30-year fixed-rate mortgages accounted for 73.9% of new originations in the U.S., according to the Urban Institute. Meanwhile, adjustable-rate mortgages only accounted for 1.1% of new loan originations in August 2020. In September 2020, the median sales price for new homes sold was $326,800 based on data from the U.S. If this is the value of your home, you must save a down payment worth $65,360.

The APR includes interest as well as the upfront fees and points you pay for a loan, as well as mortgage insurance . The property will also need to be approved by the mortgage insurer if you are putting less than a 20% down payment. Your income, credit score, and debt, and any other financial information will be re-verified, and the specific type of mortgage product that youve decided on will be factored into the equation. According to Ellie Mae, as of July 2017, mortgage lenders approved 70.6 percent of loan applications started during the previous 90 days.

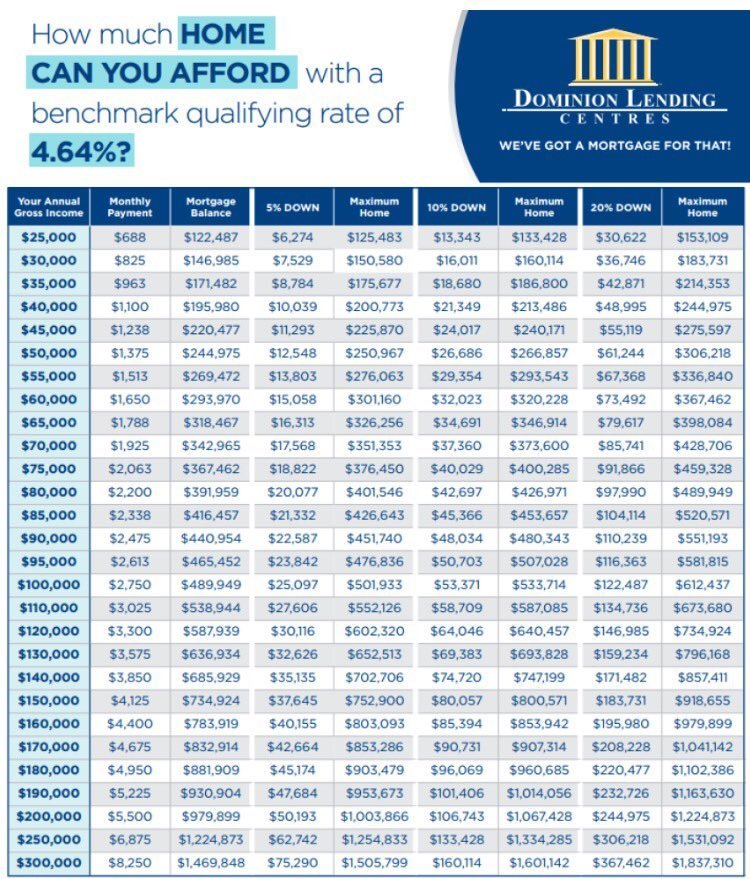

Enter the minimum required and not any higher amount you might voluntarily make. Your debt-to-income ratio also considers auto loans, minimum credit card payments, installment loans, student loans, alimony, child support, and any other expenses you must make each month. If your family earned $60,000 per year ($5,000 per month) and you had zero debts, the maximum monthly mortgage payment that most lenders might approve you for is $2,150 ($5,000 x 0.43).

No comments:

Post a Comment